In a sliding market, Stratasys has defied the odds, trading up to $9.80 per share. Its 25% gain since October 2024 has outpaced the S&P 500’s 1.7% drop. This run-up might have investors contemplating their next move.

Is now the time to buy Stratasys, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Despite the momentum, we're swiping left on Stratasys for now. Here are three reasons why we avoid SSYS and a stock we'd rather own.

Why Do We Think Stratasys Will Underperform?

Born from the Founder’s idea of making a toy frog with a glue gun, Stratasys (NASDAQ:SSYS) offers 3D printers and related materials, software, and services to many industries.

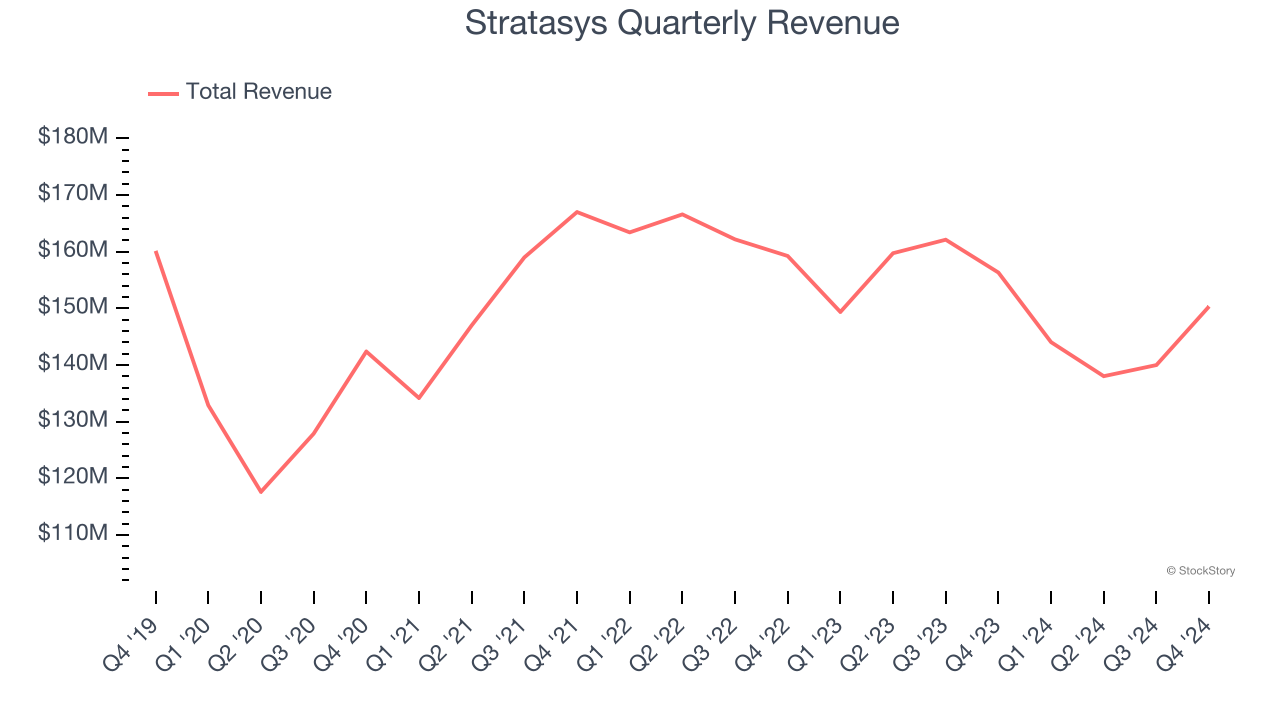

1. Revenue Spiraling Downwards

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Stratasys’s demand was weak and its revenue declined by 2.1% per year. This was below our standards and is a sign of poor business quality.

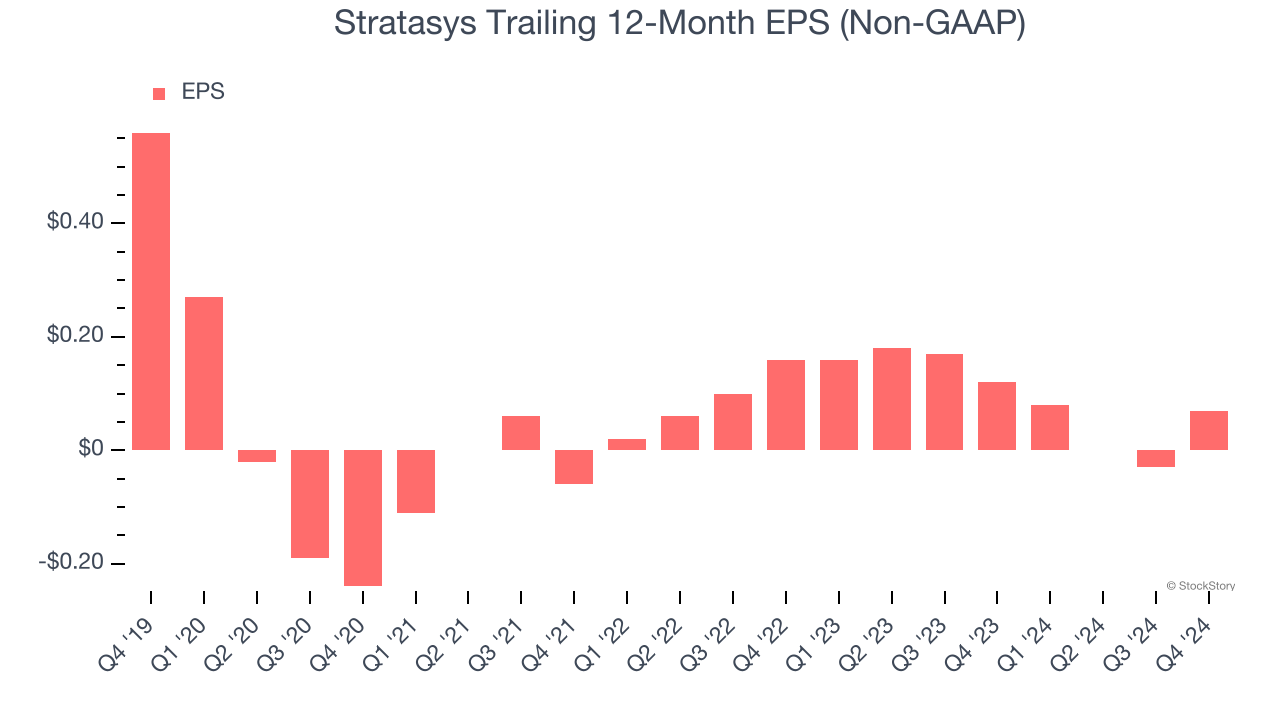

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Stratasys, its EPS declined by 34% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

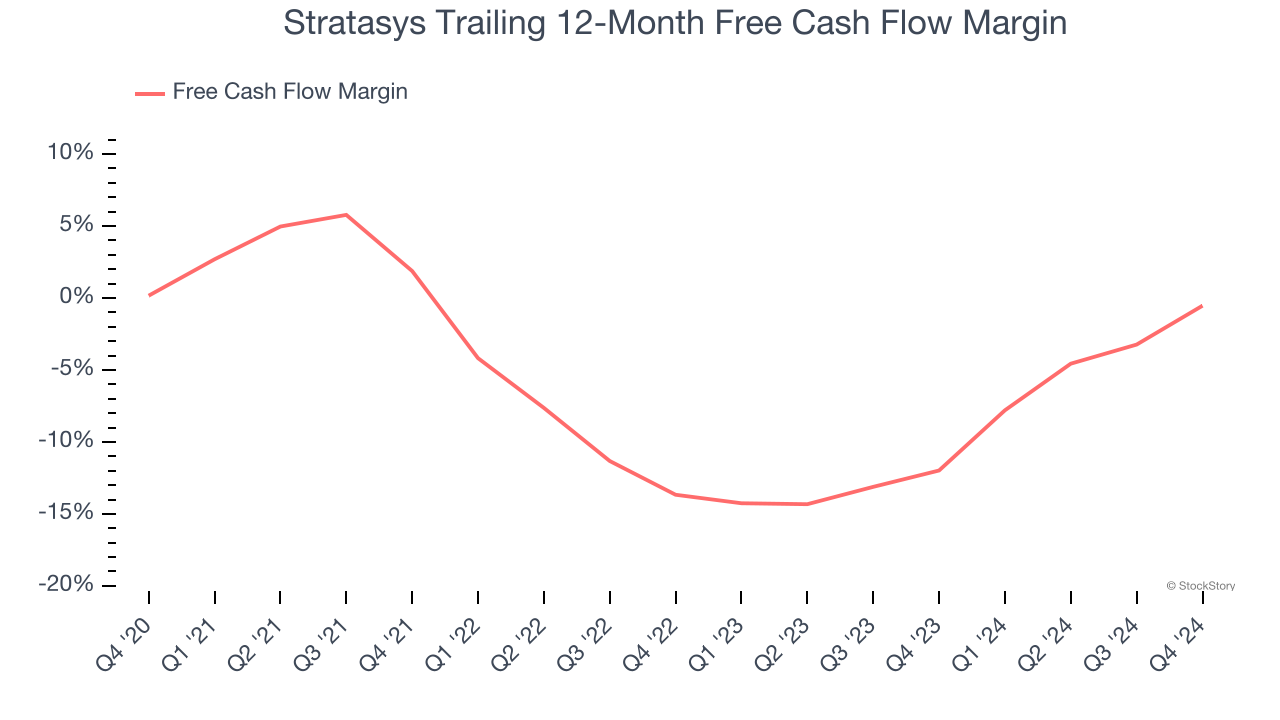

3. Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Stratasys posted positive free cash flow this quarter, the broader story hasn’t been so clean. Stratasys’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 5.2%, meaning it lit $5.20 of cash on fire for every $100 in revenue.

Final Judgment

We see the value of companies helping their customers, but in the case of Stratasys, we’re out. With its shares topping the market in recent months, the stock trades at 28× forward price-to-earnings (or $9.80 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of Stratasys

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.